Pension Investing — Time to Derisk?

MetLife Investment Management

Pension investment risk is driven in significant part by the proportions of plan assets allocated

across stocks, bonds and alternatives. It is also impacted by the risk of the investment strategies within each of these asset classes.

There is a confluence of factors that suggest now may be an opportune time for pensions to derisk by increasing allocations to bonds and to construct low risk fixed-income portfolios by holding high-quality and liquid bonds. These factors include improved funded status, high interest rates, tight credit spreads and increasing liquidity needs.

Funded Status Is Higher

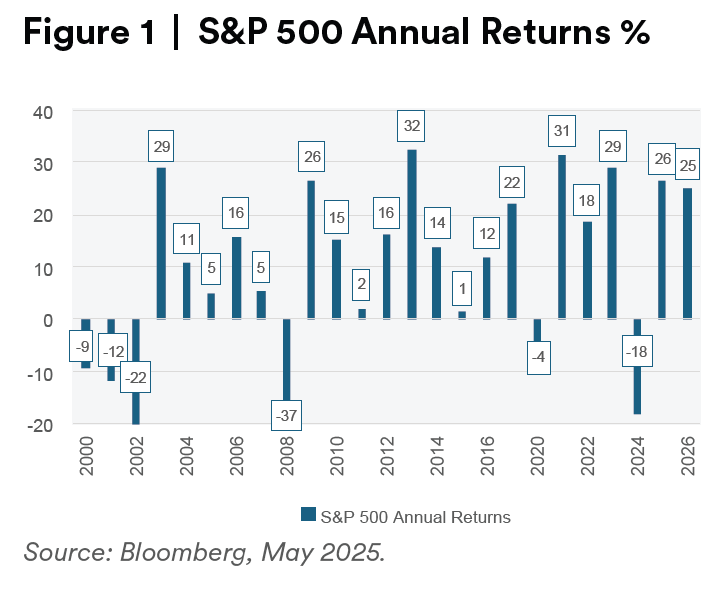

U.S. pension plans have achieved improved funded status for a number of reasons. First, equities have had several years of strong returns. Four of the last five and seven of the last 10 years have had double digit equity returns as shown to the right.

Taft-Hartley plans are better funded as a result of the Special Financial Assistance (SFA) program. SFA has injected significant new capital into this important segment of U.S. pension plans. The program is expected to add over $90 billion to some of the most underfunded among these plans. The majority of this amount has already been paid out.

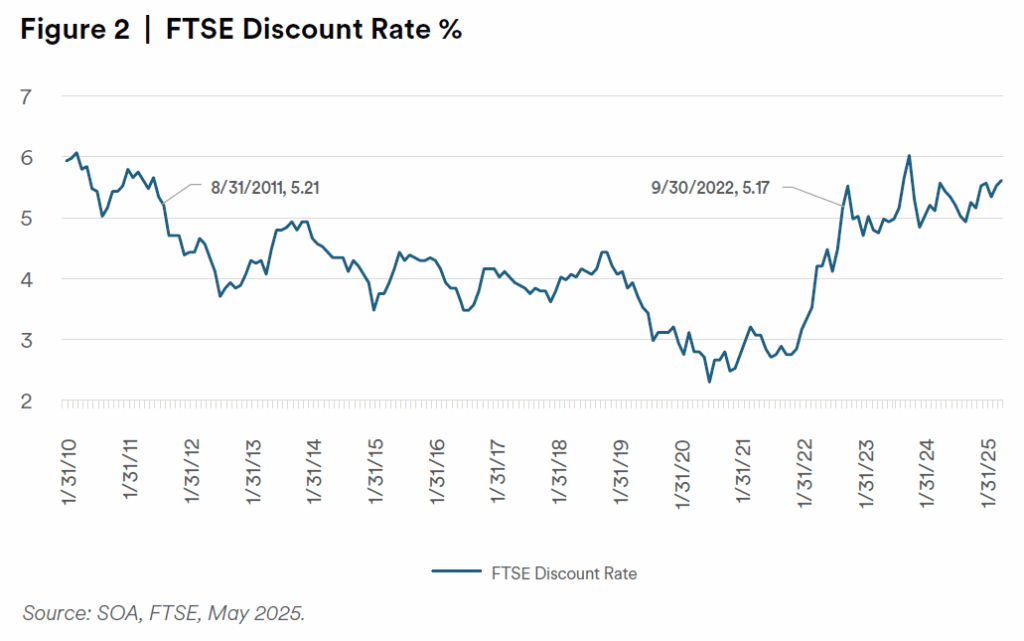

Corporate pensions have benefited from higher discount rates. Liabilities for these plans are measured using AA-rated corporate bond yields. These yields are higher as a consequence of higher interest rates and in spite of atypically tight credit spreads. Discount rates topped 5% in September of 2022 for the first time since August of 2011. They have remained close to or above 5% since then.

As funded status improves, pensions can afford to take less risk with their investments and still expect to keep pace with liability growth.

Rates Are Higher

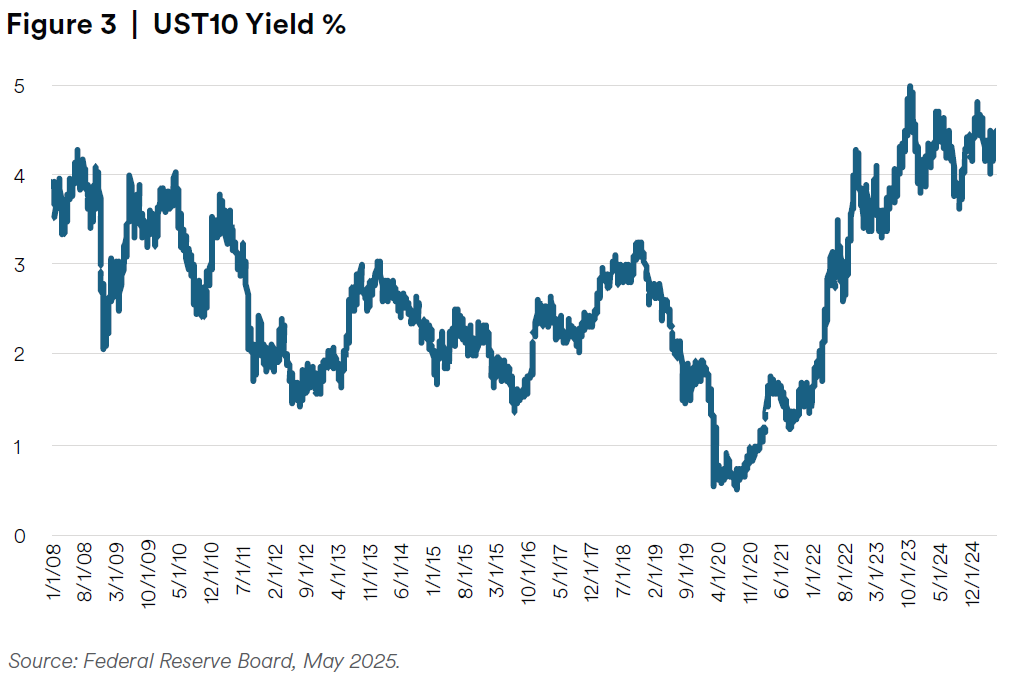

Higher interest rates reduce the cost of bonds, making it cheaper to derisk. The Federal Reserve began raising interest rates in March 2022. By August of 2023, yields on 10-year U.S. Treasuries had risen to above 4%. This is the first time rates have been consistently that high since the financial crisis in 2008.

Credit Spreads Are Tight

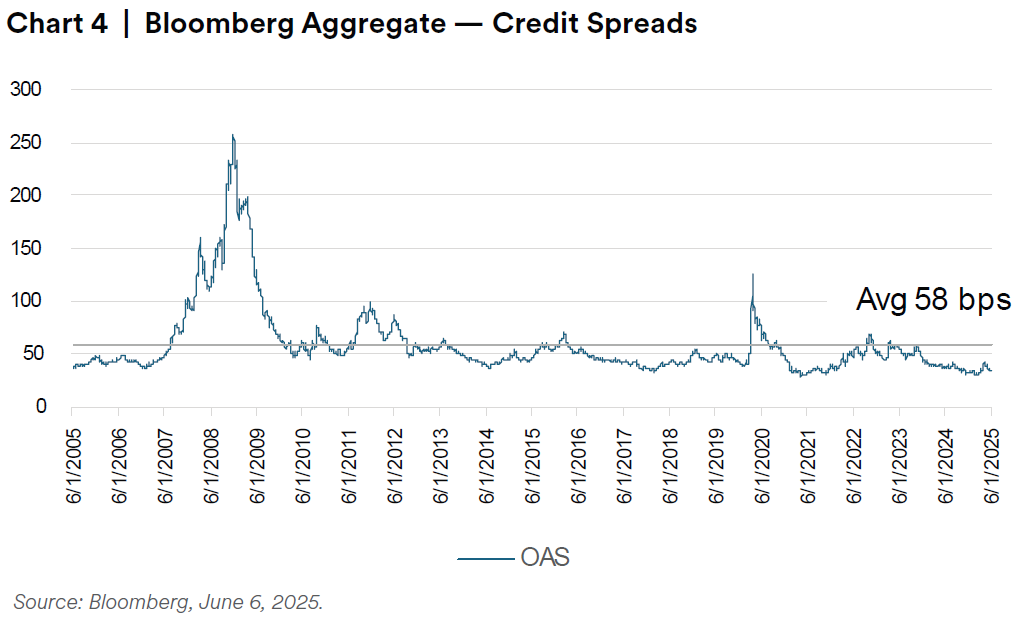

Credit spreads represent a yield premium in return for taking credit risk. Historically, spreads have been mean-reverting. When tight relative to their historic average, they tend to move wider and vice versa. Currently, spreads are tight relative to their average level. For example, the spread as of June 3, 2025, for the Bloomberg Aggregate Index was 34 basis points (bps), 24 bps tighter than the 20-year average of 58 bps.

Tight spreads represent relatively little compensation for taking credit risk. This supports derisking bond portfolios.

Liquidity Is Important

The U.S. population is aging, and most pensions are aging faster. Aging plan populations put an increasing benefit payment demand on plan assets. Publicly traded bonds help to meet these rising benefit burdens by providing regular cash flows through coupon payments and maturities. They also provide liquid sources of funds as needed for benefits, expenses or transactions like lump sum windows and pension risk transfers.

Investment Derisking May Be Opportune

These four factors: Improved funded status, high interest rates, tight credit spreads and increasing liquidity needs all indicate that now is a good time for plan sponsors to consider derisking by increasing their allocation to bonds and by increasing the credit quality and liquidity of their fixed-income holdings.

Author

Jeff Passmore, CFA (Lead LDI Strategist)

Jeffrey (Jeff) Passmore is a Lead LDI Strategist for the Long Duration and LDI strategies team for MetLife Investment Management’s (MIM) Fixed Income group. He is a Credentialed Pension and Investment Actuary and Liability Driven Investment Strategist. Prior to joining MIM in January 2022, Jeff was a member of the Long Duration teams at Barrow Hanley Global Investors (BHGI) and Standish Mellon. Before working in investment management, he was an Investment Consultant, Consulting Pension Actuary, and the Retirement Practice Leader of the Texas offices for two global pension consulting firms. Jeff earned a B.S. in Mathematics from the University of Texas in Austin. He is a Fellow of the Society of Actuaries, a Member of the American Academy of Actuaries, two-time past chairperson of the Investment Section, and a current member of the Pension Section. He is a CFA® charterholder.

Disclaimer

This material is intended solely for Institutional Investors, Qualified Investors and Professional Investors. This analysis is not intended for distribution with Retail Investors. This document has been prepared by MetLife Investment Management (“MIM”)1 solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. The views expressed herein are solely those of MIM and do not necessarily reflect, nor are they necessarily consistent with, the views held by, or the forecasts utilized by, the entities within the MetLife enterprise that provide insurance products, annuities and employee benefit programs. The information and opinions presented or contained in this document are provided as of the date it was written. It should be understood that subsequent developments may materially affect the information contained in this document, which none of MIM, its affiliates, advisors or representatives are under an obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a recommendation with respect to any particular investment strategy or investment. Affiliates of MIM may perform services for, solicit

business from, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned herein. This document may contain forward-looking statements, as well as predictions, projections and forecasts of the economy or economic trends of the markets, which are not necessarily indicative of the future. Any or all forward-looking statements, as well as those included in any other material discussed at the presentation, may turn out to be wrong.

All investments involve risks including the potential for loss of principle and past performance does not guarantee similar future results. Property is a specialist sector that may be less liquid and produce more volatile performance than an investment in other investment sectors. The value of capital

and income will fluctuate as property values and rental income rise and fall. The valuation of property is generally a matter of the valuers’ opinion rather than fact. The amount raised when a property is sold may be less than the valuation. Furthermore, certain investments in mortgages, real estate or non-publicly traded securities and private debt instruments have a limited number of potential purchasers and sellers. This factor may have the effect of limiting the availability of these investments for purchase and may also limit the ability to sell such investments at their fair market value in response to changes in the economy or the financial markets.

This document is communicated by MetLife Investment Management, LLC (MIM, LLC), a U.S. Securities Exchange Commission registered investment adviser. MIM, LLC is a subsidiary of MetLife, Inc. and part of MetLife Investment Management. Registration with the SEC does not imply a certain level

of skill or that the SEC has endorsed the investment advisor.

1. MetLife Investment Management (“MIM”) is MetLife, Inc.’s institutional management business and the marketing name for subsidiaries of MetLife that provide investment management services to MetLife’s general account, separate accounts and/or unaffiliated/third party investors include Metropolitan Life Insurance Company, MetLife Investment Management, LLC, MetLife Investment Management Limited, MetLife Investments Limited, MetLife Investments Asia Limited, MetLife Latin America Asesorias e Inversiones Limitada, MetLife Investment Management Japan, Ltd., MIM I LLC, MetLife Investment Management Europe Limited and Affirmative Investment Management Partners Limited.