Infrastructure Debt: A Compelling Private Credit Portfolio Addition

MetLife Investment Management

Executive Summary

Infrastructure debt is a growing investment opportunity where McKinsey has identified a need for US$106 trillion of infrastructure investment by 2040.1 MetLife Investment Management (“MIM”) believes infrastructure debt can be an attractive addition to a private credit strategy based on the potential for the enhanced risk adjusted return it provides, strong performance through credit cycles, and structural enhancements that act to mitigate risk relative to other high yield credit alternatives. The unique characteristics of infrastructure debt include lower default and loss rates than similarly rated corporate debt due to structural protections, collateral, and liquidity requirements and lower correlation to GDP-linked asset classes like equities and corporate debt. Infrastructure debt is a private, specialized asset class that provides exposure to several growing sectors including power and energy, digital, and transportation which continue to be supported by current economic trends. MIM has been investing in infrastructure debt since the early 1990s for its corporate parent and through its ~US$40 billion portfolio of debt and network of banks and sponsors can provide access to a vast array of infrastructure debt investments to its investment management clients.

Introduction to Infrastructure Investing

Infrastructure emerged as an investable asset class in the late 1980s and early 1990s as governments privatized public utilities and transportation assets to recycle the funds into new government spending and projects. In 2025 alone there has been over US$200 billion2 raised across over 80 funds. Supporting the deployment of this equity capital into new greenfield projects and existing brownfield projects is private debt capital. Historically, debt was provided to infrastructure projects primarily by commercial banks (90%+ pre-2008)3. However, with increased banking regulation after the global financial crisis and the growth in private credit, non-bank lending to infrastructure has grown significantly and in 1H2025 non-bank lenders made up 53% of the private debt provided to infrastructure projects.4 The need for private capital to meet the US$106 trillion of funding McKinsey5 estimates is needed by 2040 for infrastructure is supported by the continuing trends of stressed government budgets, increased mobility, growth in digitalization, and the continued transition to new and cleaner sources of energy.

Any discussion of infrastructure investing should start with a clear understanding of what “infrastructure” is meant to encompass as part of an investment strategy. At MIM, investible infrastructure means “a physical asset or system that provides an essential service to support the public or the economy with limited competition and/or high barriers to entry.”6 The fundamental characteristics of this definition of infrastructure are what differentiate debt issued by these projects from typical corporate debt:

- Physical asset or system: Long-lived, proven technology provides a long-term source of cash flow, risk

mitigation and collateral. - Essential services: The essentiality of the services limits the correlation to more GDP-linked asset classes

exposed to recessionary downturns, due to the inelastic demand for the services provided by the asset (e.g., water, power, transportation) to the public served. - Limited competition/high barriers to entry: Limited competition from natural monopolies, government

regulations or contractual arrangements support stability of demand and cash flows.

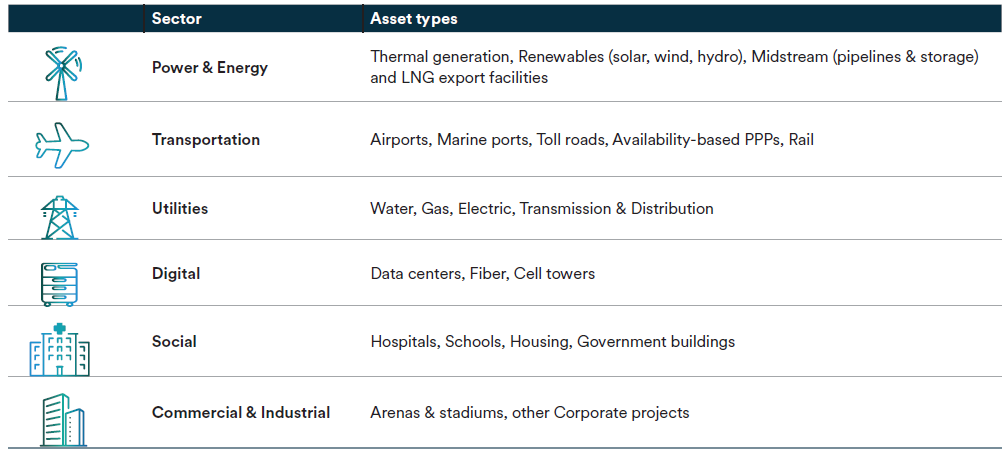

Infrastructure Sectors and Asset Types

The Infrastructure Debt team at MIM focuses on all major sectors of the infrastructure market. There are a number of asset types and new asset types continuing to emerge (e.g., renewables in power and data centers in digital). However, the analysis of each investment is based on the same fundamental risk assessment of the asset and the cash flows it will generate. At MIM, we organize infrastructure assets into six major sectors based upon asset types as follows:

Infrastructure Strategies and Risk Level

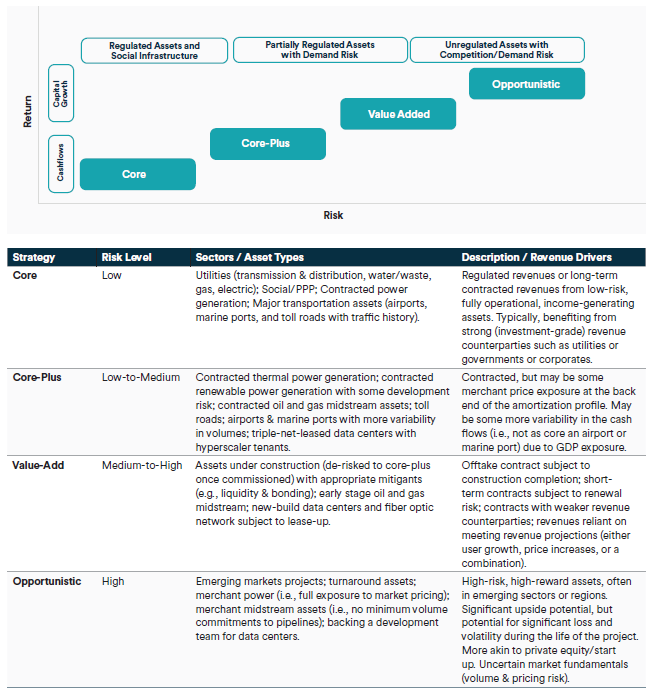

The infrastructure market typically groups investment strategies into four categories of increasing risk and return: Core, Core-Plus, Value-Added and Opportunistic. The increased risk is related to the increased uncertainty that projected cash flows will be generated. Core investors typically purchase assets that generate stable, predictable, regulated cash flows where their low cost of capital allows them to accept a lower return. At the opposite end of the spectrum is the Opportunistic strategy where investors seek higher returns by backing earlier-stage projects or development teams in hopes to capture significant upside. MIM’s infrastructure debt strategy is focused primarily on Core and Core-Plus sponsors and Value-Added sponsors where there is significant risk mitigation due to the unique features of infrastructure debt.

Infrastructure Debt Key Attributes

Private high-yield infrastructure debt has several attractive features that support its addition to a portfolio. Key attributes include: (1) enhanced cash returns that benefit from illiquidity and structural premia versus liquid public high-yield bonds; (2) lower credit risk than similarly rated corporate debt; (3) enhanced structural protections; and (4) diversification and lower correlation with typical corporate issuers.

Enhanced Cash Returns

While not indicative of future performance, in 2025, private high-yield BB infrastructure credit spreads have typically started in the high 200s to low 300s-basis-point range over the secured overnight financing rate (“SOFR”)7 for a yield of approximately 7.00% or higher.8 This has compared favorably to the BB US High Yield

Index option-adjusted spread which has averaged approximately 185 basis points through October 2025.9 Higher infrastructure spreads generally reflect investors’ need to be compensated for illiquidity and single asset risks associated with infrastructure and project finance debt. Another reason infrastructure investors are able to access higher-yielding credits is that, unlike the high-yield index, private lenders can target wider returning sectors, such as digital infrastructure or midstream, versus the over-represented utility credits. Also, while infrastructure issuers typically pay a higher rate for debt, the past record of such issuers suggests that their credit risk has actually been lower than that of corporate borrowers.

Lower Credit Risk than Similarly Rated Corporate Debt

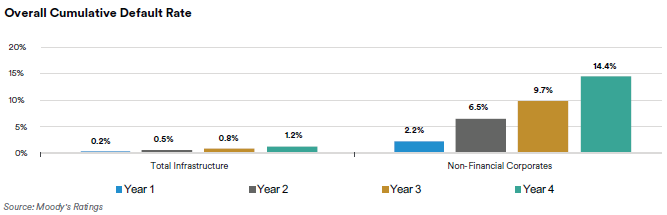

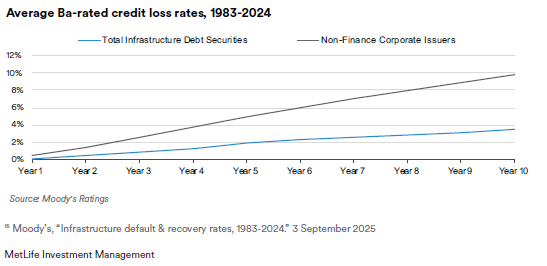

A highlight of infrastructure debt is the credit resiliency it has demonstrated through various cycles with lower default rates and lower loss rates than non-financial corporate debt. A recently updated study by Moody’s of debt securities from 1983 through 2024 showed that infrastructure debt experienced significantly lower defaults and credit losses, when compared to non-financial corporate debt between 1983 and 2024. On average, 0.8% of total infrastructure debt securities have defaulted over a five-year horizon, compared with 9.7% of non-financial corporates, and this gap only increased over time.10 Especially relevant for this yield-based infrastructure debt strategy is the difference between high-yield (BB) infrastructure debt and high-yield (BB) non-financial corporates with maturities of five years and less, given the typically shorter maturities of high-yield debt. In the BB ratings category, non-financial corporate debt’s cumulative default rates at five years are at 7.9%, compared to 4.6% for infrastructure debt or 71% higher for non-financial corporates.11 Not only does infrastructure debt experience lower defaults, but it also has a history of lower losses than non-financial corporate debt, according to the Moody’s study. The average recovery rate, based on trading prices, for senior secured infrastructure debt was 67%,12 compared to 56% for non-financial corporate issues, and an 18-year average recovery rate of 40% for high-yield bonds and 59% for leveraged loans.13 Furthermore, infrastructure debt demonstrated a loss rate at the five-year horizon that was 60% lower than similarly rated BB quality non-financial corporate debt, as the loss rate at the five-year horizon for infrastructure debt was 1.95%, compared to non-financial corporate debt of 4.91%.14 7

Enhanced Structural Protections

Infrastructure debt has structural features that also help limit defaults and support higher recovery rates. Compared to other sectors of the capital markets, infrastructure debt is highly structured with a comprehensive set of covenants that restrict a borrower’s ability to undertake actions adverse to the lender’s interests. Typical restrictions include limitations on additional indebtedness, the need to maintain debt service coverage ratios and limit leverage ratios, both to avoid a default and before any distributions are permitted to be made to equity. This ensures an alignment of interests with the equity owners. Reserves for debt services as well as major maintenance are often included as part of the debt structure. Similar to real estate, the physical infrastructure asset itself is often pledged as collateral to secure the debt, which helps explain the favorable historical recovery statistics.

Diversification & Lower Correlations with Corporate Issuers

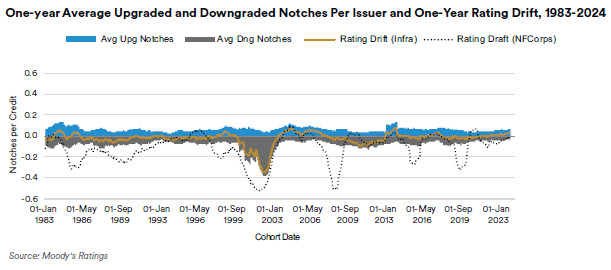

In addition to lower default rates and lower losses, Moody’s study also showed that ratings volatility for infrastructure debt has been “near zero” for much of the study period outside of the energy crisis in the early 2000s, as shown in the exhibit below.15 These economic shocks were demonstrated during the Global Financial Crisis in 2008–2009, during the energy price drop in 2015–2016, and most recently, during the COVID-19 shutdown in 2020–2021. Infrastructure assets’ ability to withstand economic cyclicality is attributable to the essentiality of the services they provide, as well as the structural features of the debt instruments, which typically require liquidity in the form of debt service reserves in the event there is some type of event or operating issue that interrupts the normal projected generation of cash flows. Also, infrastructure assets often benefit from revenue contracts that are indexed to inflation, so that as costs increase, their revenues step up with the Consumer Price Index or some other form of indexation. Finally, lower correlation relates to the unique revenue drivers of the infrastructure assets, such as contracts or regulatory regimes that are often not linked to the performance of the broader economy or consumer spending.

MetLife Investment Management’s Approach to Infrastructure Debt

Origination Access & Market Reach

MIM was named the largest infrastructure debt investor globally in 2024 by Investment & Pensions Europe. Institutional investing in infrastructure significantly increased beginning in 2009 when banks pulled back from the sector during the Global Financial Crisis. MIM manages US$39.6 billion in infrastructure debt across over 400 credits in power & energy, transportation, utilities, digital, social, and commercial & industrial sectors. The firm’s 20-person global infrastructure debt team, located in the US, UK, and Chile, leverages these ties to access differentiated deal flow on behalf of its clients.

Credit Discipline & Rigorous Underwriting

As a balance sheet investor, MIM focuses first and foremost on capital preservation and stable, consistent, risk adjusted cash returns and not short-term paper gains. MIM applies fundamental asset analysis to sub-investment grade exposures including in depth due diligence, detailed cash-flow modeling, covenant structuring and review with counsel as well as collateral evaluation. Deals that are written up are then subjected to review by a credit committee process consisting of senior members from across the Private Fixed Income group, including the Infrastructure Debt team.

Integrated ESG Research & Cross-Platform Insights

The infrastructure credit process includes a review of financially material Environmental, Social, and Governance (ESG) related risks and opportunities as part of underwriting for every deal. The Private Credit Sustainability Research team sits alongside the Infrastructure Debt team in MIM’s London office and is available to provide dedicated sustainability expertise as required. In addition to the Sustainability Research team’s ESG contributions, the Infrastructure Debt team also benefits from access to the insights and expertise of the Corporate Private Placement and Private Asset Backed Finance teams, all of which are part of the unified Private Fixed Income group. Furthermore, MIM’s Real Estate teams also serve as a resource in the digital infrastructure and other logistics related areas where infrastructure and real estate overlap. The Infrastructure Debt team has the full benefit of MIM’s standing as a multi-asset class global asset

manager.

Risks to Consider

Investment in private infrastructure debt offers many benefits, but like all other investments, there are risks to consider, such as the ones listed below.

Illiquidity

Private infrastructure debt is an illiquid asset class with no readily tradeable market. Therefore the investment asset may not easily be sold. The Moody’s recovery study indicated that ultimate recoveries (i.e., being able to hold the investment to ultimate resolution) may outperform trading recoveries. This illiquidity may limit an investor’s ability to redeem their investment. Including infrastructure debt as part of a long-term investment strategy, while maintaining adequate levels of liquidity on a portfolio-wide basis, is one way to manage illiquidity risk at the portfolio level.

Legal/Regulatory Risk

Legal and/or regulatory changes could be implemented or imposed that could have a negative impact on the cash flows of a project due to increased costs related to remediation, fines or loss of permits or licenses. Failure to comply with laws, statutes and regulations could result in fines or shutdowns of projects, which would also potentially have material impact on the cash flows of the project. It is important to assess these risks when analyzing an investment and to ensure that the appropriate professionals and legal support are utilized to understand the critical issues involved.

Operating/Technology Risk

Infrastructure assets are often complex and require maintenance and technical upkeep. Ongoing operations and maintenance (O&M) by qualified personnel and a sufficient budget to meet operating needs are critical to the successful generation of projected cash flows by an infrastructure asset. Assets occasionally have operating issues, and appropriate staffing or response plans for any unforeseen problems are necessary to ensure the continued operation of projects. Ways to mitigate operating issues include proper staffing of projects with qualified personnel, ensuring proper insurance is maintained, requiring maintenance reserves in the debt structure and proper assignment of risk (e.g., technical risk to the provider of the technology through a warranty and operating risk to the operator through KPI penalties).

Blind Pool Risk

Investing in an infrastructure debt strategy where the manager has a set of investment criteria, but otherwise has discretion, means investors are essentially committing to “blind pools.” Investors must commit to fund the pool’s future investments without knowing what they are to be. Investors risk that the manager may diverge from what the investors understood the marketed strategy to be. The use of stated criteria for inclusion into the pool is a partial mitigant to complete discretion but remains subject to the manager’s ultimate interpretation of the criteria. There is a risk that the manager may construct a portfolio differently than was anticipated by the investor.

Environmental Risk

Infrastructure investments sometimes involve environmental risks. Potential consequences of an environmental issue could be fines, regulatory changes and contamination — all of which may negatively affect operating performance. Proper compliance with a sound operating plan and laws and regulations can mitigate potential environmental issues. Any contamination associated with a project could ultimately become the financial burden of that project.

Author

Patrick Manseau, Managing Director, Private Capital

References

1 McKinsey & Company, “The Infrastructure Moment: Investing in the expanding foundations of modern society” by Alastair Green, Ishaan Nangia, Nicola Sandri, September 2025

2 IJ Global

3 Infrastructure Debt—Understanding the Opportunity.pdf

4 IJ Global, Infrastructure and Project Finance League Table Report H1 2025 (Infrastructure and Project Finance Charts)

5 McKinsey & Company, 6 “The Infrastructure Moment: Investing in the expanding foundations of modern society” by Alastair Green, Ishaan Nangia, Nicola Sandri, September 2025

7 MetLife Investment Management, LLC observed data

8 This is not intended to serve as investment advice and past performance is not indicative of future performance.

9 BAMLH0A1HYBB (2024-10-10 to 2025-10-10)

10 Moody’s, “Infrastructure default & recovery rates, 1983-2024.” 3 September 2025

11 Moody’s, “Infrastructure default & recovery rates, 1983-2024.” 3 September 2025

12 Moody’s, “Infrastructure default & recovery rates, 1983-2024.” 3 September 2025

13 Cliffwater Report on U.S. Direct Lending (2023 Q3). Source: JPMorgan Markets, Bloomberg US High Yield Index, Morningstar LSTA Leveraged Loan Index.

14 Moody’s, “Infrastructure default & recovery rates, 1983-2024.” 3 September 2025

Disclosure

This document has been prepared by MetLife Investment Management, LLC, a U.S. Securities and Exchange Commission (SEC) registered investment adviser. Registration with the SEC does not imply a certain level of skill or that the SEC has endorsed the investment adviser.

The firm is part of MetLife Investment Management (MIM), which is MetLife Inc.’s institutional investment management business. MIM is a group of international companies that provides investment advice and markets asset management products and services to clients around the world. The various global teams referenced in this document, including portfolio managers, research analysts and traders are employed by the various legal entities that comprise MIM.

No money, securities or other consideration is being solicited. This document has been provided to you solely for informational purposes and does not constitute a recommendation regarding any investments or the provision of any investment advice, or constitute or form part of any advertisement of, offer for sale or subscription of, solicitation or invitation of any offer or recommendation to purchase or subscribe for any securities or investment advisory services. Subsequent developments may affect the information contained in this document materially, and MIM shall not have any obligation to update, revise or affirm. It is not MIM’s intention to provide, and you may not rely on this document as providing, a complete or comprehensive analysis of MIM’s investment portfolio, investment strategies or investment recommendations.

Confidentiality. This document and the information contained herein is strictly confidential (and by receiving such information you agree to keep such information confidential) and are being furnished to you solely for your information and may not be used or relied upon by any other party, or for any other purpose, and may not, directly or indirectly, be forwarded, published, reproduced, disseminated or quoted to any other person for any purpose without the prior written consent of MIM. This reminder should not be read to limit, in any way, the terms of any confidentiality agreement you or your organization may have in place with MIM. Any forwarding, publication, distribution or reproduction of this document in whole or in part is unauthorized. Any failure to comply with this restriction may constitute a violation of applicable securities laws. Risk of loss. An investment in the strategy described herein is speculative and there can be no assurance that the strategy’s investment objectives will be achieved. Investors must be prepared to bear the risk of a total loss of their investment. Your capital is at risk, investing in the strategies discussed herein are subject to various risks which must be considered prior to investing. No tax, legal or accounting advice. This document is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations. Any statements of U.S. federal tax consequences contained in this document were not intended to be used and cannot be used to avoid penalties under the U.S. Internal Revenue Code or to promote, market or recommend to another party any tax-related matters addressed herein.

Forward-Looking Statements. This document may contain or incorporate by reference information that includes or is based upon forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements give expectations or forecasts of future events. These statements can be identified by the fact that they do not relate strictly to historical or current facts. They use words and terms such as “anticipate,” “estimate,” “expect,” “project,” “intend,” “plan,” “believe,” “will,” and other words and terms of similar meaning, or are tied to future periods in connection with a discussion of future performance. Forward-looking statements are based upon MIM’s assumptions and current expectations, which may be inaccurate, and on the current economic environment which may change. These

statements are not guarantees of future performance. They involve a number of risks and uncertainties that are difficult to predict. Results could differ materially from those expressed or implied in the forward-looking statements. Risks, uncertainties and other factors that might cause such differences include but are not limited to: (1) difficult conditions in the global capital markets; (2) changes in general economic conditions, including changes in interest rates or fiscal policies; (3) changes in the investment environment; (4) changed conditions in the securities or real estate markets; and (5) regulatory, tax and political changes. MIM does not undertake any obligation to publicly correct or update any forward-looking statement if it later becomes aware that such statement is not likely to be achieved.

For investors in Australia: This information is distributed by MIM LLC and is intended for “wholesale clients” as defined in section 761G of the Corporations Act 2001 (Cth) (the Act). MIM LLC exempt from the requirement to hold an Australian financial services license under the Act in respect of the financial services it provides to Australian clients. MIM LLC is regulated by the SEC under US law, which is different from Australian law.

10-27 4899297-[MIM, LLC (US)]